Daftar Isi:

How do insurance companies determine premiums? It’s a question that’s probably crossed your mind at some point, especially when you’re comparing quotes or getting ready to renew your policy. Think of it like a game of risk and reward – insurance companies are in the business of assessing your likelihood of needing a payout, and they use a whole bunch of factors to figure out how much you’ll pay each month.

From your driving history and credit score to your age, location, and even your occupation, insurance companies gather information to create a unique profile of your risk. They analyze data, use statistical models, and consider a whole lot of factors to make sure they’re charging you a fair price based on your chances of needing to file a claim.

Risk Assessment and Premium Determination

Insurance companies, those superheroes of financial security, don’t just hand out policies like candy. They’re in the business of managing risk, and that means carefully assessing who they’re insuring and how much they should charge.

Underwriting: The Risk Whisperers

Underwriting is the process of evaluating risk, and it’s like a detective’s investigation. Insurance companies have a team of underwriters who dig deep into your background, looking for clues about your potential for making a claim. They want to understand your risk profile, and they use that information to determine your premium.

Risk Factors: The Ingredients of Your Premium

Think of your premium as a custom-made cocktail, with different ingredients affecting the final taste. Here are some common risk factors that can influence your premium:

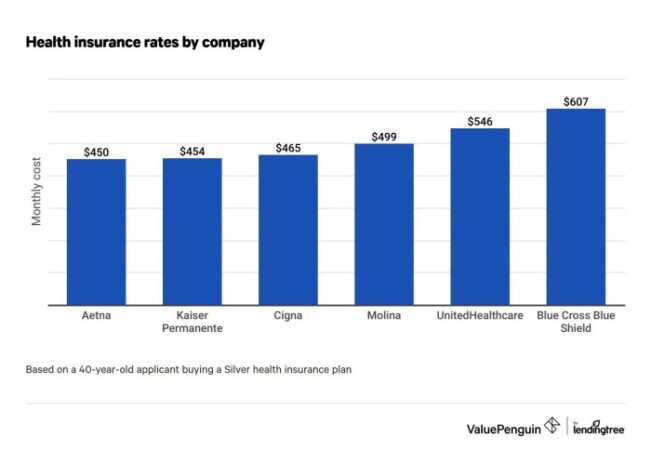

- Health Conditions: If you’re a fitness fanatic with a clean bill of health, you’ll likely pay less for health insurance than someone with pre-existing conditions. The risk of needing medical care is higher for those with health issues, so insurers adjust premiums accordingly.

- Driving History: Got a clean driving record? Congratulations! You’re probably going to get a lower premium on your car insurance. But if you’ve got a few speeding tickets or a fender bender in your past, your premiums might be a bit higher.

- Property Location: Location, location, location! Insurance companies consider where you live when setting premiums. A home in a high-crime area might have higher premiums than a home in a safe neighborhood. Similarly, if your house is located in an area prone to natural disasters like earthquakes or floods, your insurance rates might be higher.

- Lifestyle: Some insurers consider your lifestyle when setting premiums. For example, if you’re a thrill-seeker who enjoys extreme sports, your insurance rates might be higher than someone who prefers a more relaxed lifestyle.

The Risk Assessment Process: A Flowchart

Imagine the risk assessment process as a journey, with each step leading you closer to your final premium:

[Flowchart illustration]

The flowchart illustrates how an insurance company assesses risk, starting with the initial application and moving through data collection, analysis, and the final premium determination.

Premium Adjustments and Discounts: How Do Insurance Companies Determine Premiums

Insurance premiums are not set in stone. Insurance companies use a variety of factors to determine your premium, and these factors can change over time. This means that your premium may go up or down depending on a number of things.

Premium Adjustments Based on Policy Changes

Insurance companies adjust premiums based on policy changes to ensure that the premium accurately reflects the risk they are taking on. If you make changes to your policy, such as adding or removing coverage, your premium will be adjusted accordingly.

For example, if you add collision coverage to your car insurance policy, your premium will likely increase. This is because collision coverage protects you from damage to your car in an accident, which increases the risk for the insurance company. Conversely, if you remove collision coverage, your premium will likely decrease.

Common Discounts, How do insurance companies determine premiums

Insurance companies offer a variety of discounts to encourage policyholders to take steps to reduce their risk. Some common discounts include:

- Safe Driving Discount: This discount is offered to drivers with a clean driving record, typically for a certain number of years without any accidents or traffic violations.

- Good Student Discount: This discount is offered to students who maintain a certain grade point average (GPA). This discount is based on the idea that good students are more responsible and less likely to engage in risky behavior.

- Multi-Policy Discount: This discount is offered to policyholders who bundle multiple insurance policies, such as home and auto insurance, with the same company. This discount is based on the idea that policyholders with multiple policies are more loyal and less likely to switch companies.

Impact of Claims History

Your claims history has a significant impact on your future premiums. If you file a claim, your premium will likely increase. This is because the insurance company has to pay out a claim, which increases their risk. The higher the cost of the claim, the more your premium is likely to increase.

Conversely, if you have a clean claims history, your premium may decrease. This is because the insurance company views you as a low-risk customer.

Premium Adjustment Types

| Premium Adjustment Type | Description | Impact on Premium | Example |

|---|---|---|---|

| Policy Change | Adding or removing coverage, such as collision or comprehensive coverage. | Increase or decrease in premium based on the change. | Adding collision coverage to your auto policy will increase your premium. |

| Discount | Offered for various factors, such as safe driving, good student, and multi-policy discounts. | Reduction in premium. | A safe driving discount can lower your auto insurance premium. |

| Claims History | Filing a claim increases your risk and can lead to higher premiums. A clean claims history can lead to lower premiums. | Increase or decrease in premium based on the claim history. | Filing a claim for a car accident can increase your auto insurance premium. |

Transparency and Communication

Insurance companies are all about transparency and communication, especially when it comes to premium rates and policy details. It’s a two-way street: they need to clearly explain how they calculate your premiums, and you need to be able to understand that information to make informed decisions about your coverage.

Methods of Communication

Insurance companies use various methods to communicate premium rates and policy details to their customers.

- Websites: Most insurance companies have detailed websites with information about their policies, coverage options, and premium calculations. These websites often have online tools and calculators to help customers estimate their premiums and compare different policies.

- Brochures and Policy Documents: Insurance companies provide printed brochures and policy documents that explain the terms and conditions of their policies, including the factors that influence premium calculations. This documentation is often available both online and in physical form.

- Customer Service Representatives: Insurance companies have dedicated customer service representatives who are trained to answer questions about policies, premiums, and coverage options. They can provide personalized guidance and help customers understand their specific policy details.

- Agents and Brokers: Independent insurance agents and brokers can act as intermediaries between customers and insurance companies. They can help customers compare different policies, explain premium calculations, and provide personalized advice.

Importance of Clear Communication

Clear and concise communication regarding premium calculations is essential for building trust and ensuring customer satisfaction.

- Informed Decision-Making: Customers need to understand how their premiums are calculated to make informed decisions about their coverage needs. This includes knowing the factors that affect their premium, such as age, driving record, credit score, and location.

- Transparency and Trust: Transparent communication helps build trust between insurance companies and their customers. When customers feel confident that they understand their premiums, they are more likely to be satisfied with their policy and the company.

- Reduced Disputes and Complaints: Clear communication can help prevent misunderstandings and disputes regarding premiums. When customers understand the rationale behind their premium, they are less likely to file complaints or challenge their policy.

Tools and Resources

Insurance companies are increasingly using digital tools and resources to help customers understand their premiums.

- Online Premium Calculators: These tools allow customers to input their personal information and get an estimated premium for different policies. This can help customers compare policies and find the best coverage for their needs.

- Policy Summaries: Some insurance companies provide concise policy summaries that highlight the key features and benefits of their policies, including the factors that influence premiums. This helps customers quickly understand the essential details of their coverage.

- Interactive Tutorials and Videos: Many insurance companies are using interactive tutorials and videos to explain complex concepts like premium calculations in a simple and engaging way. These resources can help customers visualize how their premium is determined and understand the factors that contribute to it.

Sample Insurance Policy Document

Here’s an example of how a simplified insurance policy document could break down premium components:

Policyholder: John Smith

Policy Number: 1234567890

Coverage Type: Auto Insurance

Premium: $100 per monthPremium Breakdown:

* Base Premium: $50 (based on vehicle type, coverage limits, and state regulations)

* Driving Record: $15 (minor traffic violations)

* Credit Score: $10 (good credit score)

* Location: $15 (urban area with higher risk of accidents)

* Safety Features: -$10 (vehicle has anti-theft system and airbags)

This sample document provides a clear breakdown of the factors that influence John Smith’s premium. It shows the base premium, which is determined by factors like vehicle type and coverage limits, and then adds adjustments for driving record, credit score, location, and safety features. This transparent approach helps John understand how his premium is calculated and what factors influence it.

Final Thoughts

Understanding how insurance companies determine premiums is crucial for making smart decisions about your insurance. By being aware of the factors that influence your rates, you can take steps to lower your costs and ensure you’re getting the best possible coverage for your needs. So, whether you’re looking to save money on your car insurance, find a great deal on health insurance, or make sure you have the right life insurance policy, understanding how premiums are calculated is key.

Question Bank

Can I get a lower premium if I bundle my insurance policies?

Absolutely! Many insurance companies offer discounts for bundling multiple policies, like car and home insurance, together. It’s a great way to save money and simplify your insurance needs.

What happens if I make a claim?

Filing a claim will generally impact your future premiums. The severity and frequency of your claims will be taken into account when your rates are adjusted. It’s important to be mindful of how your claims history can affect your future costs.

How can I compare insurance quotes from different companies?

There are several online tools and websites that allow you to compare quotes from different insurance companies. You can also contact companies directly to get personalized quotes. It’s always a good idea to shop around and compare prices before making a decision.