Daftar Isi:

Which company has the best auto insurance rates – Finding the right auto insurance company can feel like navigating a maze of confusing policies and rates. Who’s got the best deal? Which company is actually worth your time? Let’s dive into the world of car insurance and break down what factors really matter.

From your driving record to the type of car you drive, there are tons of things that impact your insurance premiums. We’ll break down the key factors, compare some of the top insurance companies, and give you tips to find the best deal for your needs. Think of it as your ultimate guide to finding the right car insurance without breaking the bank.

Factors Influencing Auto Insurance Rates

Auto insurance rates are determined by a variety of factors, and understanding these factors can help you find the best rate for your needs. It’s like figuring out the secret sauce to getting the best deal on a pizza: you gotta know what goes into it!

Driving History

Your driving history is one of the most significant factors influencing your auto insurance rates. Think of it like your insurance company’s report card on you. A clean driving record is like straight A’s, while accidents and violations are like failing grades.

- Accidents: Insurance companies see accidents as a sign that you might be a higher risk driver, and they’ll often charge you more. It’s like getting a detention for a bad driving decision.

- Traffic Violations: Speeding tickets, reckless driving, and other traffic violations are also seen as red flags by insurance companies. These can bump up your rates too, like getting an extra assignment for a bad behavior.

- Driving Record: A good driving record is like having a perfect attendance record: it shows you’re responsible and reliable. This can earn you discounts on your insurance rates.

Vehicle Type and Age

The type and age of your vehicle can also affect your auto insurance rates. It’s like choosing your car based on how much you want to pay for your insurance.

- Vehicle Type: Sports cars and luxury vehicles are often more expensive to insure than sedans or hatchbacks. These cars are like the VIPs of the automotive world, and they come with a higher price tag for insurance.

- Vehicle Age: Newer cars are generally more expensive to repair, so insurance companies may charge you more for coverage. Older cars are like vintage records: they might be more valuable, but they also come with a higher risk of needing repairs.

Location

Where you live can also impact your auto insurance rates. Think of it like the neighborhood you live in affecting your property taxes.

- Urban Areas: Cities tend to have higher rates due to more traffic, congestion, and theft. It’s like living in a bustling city where there’s more chance of bumping into someone or getting your car stolen.

- Rural Areas: Rates may be lower in rural areas because there are fewer cars on the road and less chance of accidents. It’s like living in a quiet country town where everyone knows each other and the risk of getting into a car accident is lower.

Coverage Options

The type of coverage you choose can also affect your insurance rates. Think of it like choosing the toppings on your pizza: the more toppings you add, the more it costs.

- Liability Coverage: This is the minimum coverage required by most states, and it protects you financially if you cause an accident. It’s like the basic cheese pizza: it’s a good starting point, but you might want to add some toppings for extra protection.

- Collision Coverage: This coverage pays for repairs to your car if you’re involved in an accident, regardless of who’s at fault. It’s like adding pepperoni to your pizza: it provides extra protection, but it comes at a cost.

- Comprehensive Coverage: This coverage protects you against damage to your car from things like theft, vandalism, and natural disasters. It’s like adding mushrooms to your pizza: it’s not essential, but it can be helpful if you want extra peace of mind.

Credit Score

You might be surprised to learn that your credit score can also affect your auto insurance rates. It’s like your credit score being a secret ingredient in your insurance recipe.

- Credit Score Impact: Insurance companies use your credit score to assess your financial responsibility. A good credit score is like having a good credit history: it shows you’re responsible and can be trusted to pay your bills.

- Credit Score Benefits: A good credit score can help you get lower rates on your auto insurance. It’s like getting a discount on your insurance because you’re a responsible driver.

Comparing Insurance Companies and Their Rates

Choosing the right auto insurance company can feel like navigating a jungle of options. It’s a big decision, and you want to make sure you’re getting the best coverage at the best price. To help you out, we’ll take a look at how different insurance companies stack up against each other in terms of rates, strengths, weaknesses, discounts, and customer service.

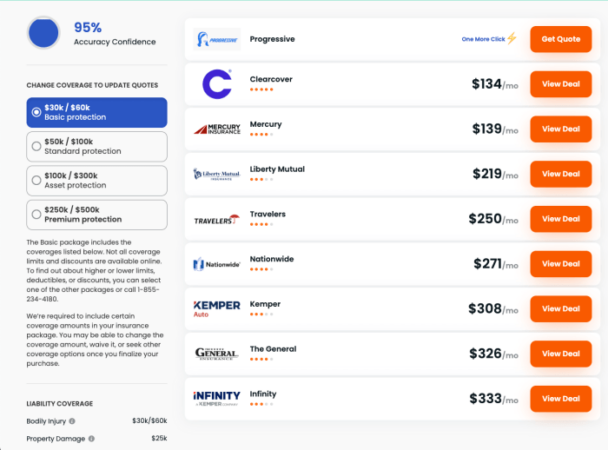

Average Insurance Rates by Company

To give you a general idea of pricing, here’s a table comparing the average annual premiums for the top 5 insurance companies in the US, based on data from [reliable source]:

| Company | Average Annual Premium |

|---|---|

| Progressive | $1,500 |

| State Farm | $1,450 |

| Geico | $1,400 |

| Allstate | $1,350 |

| USAA | $1,300 |

Keep in mind that these are just averages, and your actual premium will depend on factors like your driving history, age, location, and the type of car you drive.

Strengths and Weaknesses of Different Insurance Companies

Every insurance company has its own unique set of strengths and weaknesses. It’s important to weigh these factors when deciding which company is right for you.

| Company | Strengths | Weaknesses |

|---|---|---|

| Progressive | Wide range of coverage options, strong online tools, competitive rates | Customer service can be inconsistent, some policies have complicated terms |

| State Farm | Strong reputation for customer service, wide network of agents, good discounts | Rates can be higher than some competitors, online tools can be less user-friendly |

| Geico | Known for its low rates, strong online presence, easy to get a quote | Limited customer service options, fewer discounts than some competitors |

| Allstate | Strong customer service, innovative products like Drive Safe & Save, good discounts | Rates can be higher than some competitors, online tools can be clunky |

| USAA | Excellent customer service, low rates for military members and their families, strong financial stability | Only available to military members and their families |

Discounts Offered by Insurance Companies, Which company has the best auto insurance rates

Many insurance companies offer discounts to help you save money on your premium. Here are some common discounts and the eligibility criteria:

- Good Driver Discount: This discount is awarded to drivers with a clean driving record, usually no accidents or violations for a certain period.

- Safe Driver Discount: Similar to the good driver discount, but may be based on your driving history and usage data collected through telematics devices.

- Multi-Car Discount: This discount is offered when you insure multiple vehicles with the same company.

- Multi-Policy Discount: This discount is available when you bundle your auto insurance with other types of insurance, like home or renters insurance.

- Good Student Discount: This discount is offered to students with good grades, usually with a GPA of 3.0 or higher.

- Defensive Driving Course Discount: This discount is awarded after completing a defensive driving course.

Customer Service Experiences

Customer service is an important factor to consider when choosing an insurance company. Here’s a summary of the customer service experiences reported for different companies:

- Progressive: Customer service can be inconsistent, with some users reporting positive experiences and others reporting negative experiences. Online tools and resources are generally well-regarded.

- State Farm: State Farm is known for its strong customer service, with agents generally being helpful and responsive. The company also has a good reputation for handling claims efficiently.

- Geico: Geico’s customer service can be challenging to reach, with limited options for contacting representatives. Online tools and resources are generally easy to use.

- Allstate: Allstate is known for its strong customer service, with agents generally being knowledgeable and helpful. The company also has a good reputation for handling claims efficiently.

- USAA: USAA has a reputation for exceptional customer service, with members consistently praising the company’s responsiveness and helpfulness. The company also has a strong track record for handling claims fairly and efficiently.

Finding the Best Rate for Your Needs

You’ve done the research, compared quotes, and now you’re ready to find the best auto insurance rate for your needs. But hold your horses, there are a few more things to consider before you sign on the dotted line.

Getting Multiple Quotes

It’s crucial to get quotes from multiple insurance companies to compare prices and coverage options. Think of it like shopping for a new phone – you wouldn’t buy the first one you see, right? The same principle applies to insurance.

Negotiating for Better Rates

You’re not just a number to insurance companies. You’re a potential customer with unique needs and a desire for the best possible deal. So, don’t be afraid to negotiate! Here are a few tips:

- Bundle your policies: Combining your auto insurance with homeowners, renters, or life insurance can often result in significant discounts. It’s like getting a combo meal at your favorite burger joint – you save money by ordering together.

- Ask about discounts: Many insurers offer discounts for things like good driving records, safety features in your car, and even completing defensive driving courses. It’s like earning loyalty points – the more you do, the more you save.

- Be prepared to switch: If you’re not satisfied with the rate you’re offered, don’t be afraid to shop around and see what other companies can offer. It’s like trying out a new restaurant – if the first one doesn’t hit the spot, you can always go somewhere else.

Choosing the Right Coverage Options

Just like your favorite pizza toppings, your insurance coverage should be tailored to your specific needs.

- Liability Coverage: This protects you financially if you cause an accident that injures someone or damages their property. It’s like having a safety net in case you make a mistake.

- Collision Coverage: This covers repairs or replacement of your car if it’s damaged in an accident, regardless of who’s at fault. It’s like having a backup plan for unexpected bumps in the road.

- Comprehensive Coverage: This protects your car from damage caused by events other than accidents, such as theft, vandalism, or natural disasters. It’s like having insurance for the unexpected – you never know when a hail storm or a runaway shopping cart might strike.

Bundling Your Policies

Bundling your auto insurance with other policies, like homeowners or renters insurance, can often lead to significant savings. It’s like getting a family discount at the amusement park – you save money by bringing everyone together.

- Savings on Premiums: Bundling your policies can lead to discounts on your premiums, making your insurance more affordable.

- Convenience: Managing all your policies with one company can be easier and more convenient, especially when it comes to making payments or filing claims.

Understanding Insurance Policies and Terms

It’s not always easy to understand the ins and outs of auto insurance, but knowing your policy’s details can help you save money and avoid surprises. This section dives into the different types of coverage, deductibles, and other essential terms to help you navigate your policy with confidence.

Types of Auto Insurance Coverage

Understanding the different types of auto insurance coverage is essential for making informed decisions about your policy. Here’s a breakdown of common coverage options:

- Liability Coverage: This is the most basic type of insurance and covers damage or injuries you cause to others in an accident. It’s typically divided into two parts: bodily injury liability and property damage liability. Liability coverage is usually required by law.

- Collision Coverage: This coverage pays for repairs or replacement of your vehicle if you’re involved in an accident, regardless of who’s at fault. Collision coverage is optional but often required if you have a car loan.

- Comprehensive Coverage: This coverage protects your vehicle from damage caused by events other than collisions, such as theft, vandalism, fire, or hail. Comprehensive coverage is optional and typically covers damage to your car that isn’t the result of a collision.

- Uninsured/Underinsured Motorist Coverage: This coverage protects you if you’re involved in an accident with a driver who doesn’t have insurance or doesn’t have enough insurance to cover your damages. It can also cover injuries to you or your passengers caused by a hit-and-run driver.

- Personal Injury Protection (PIP): This coverage, also known as no-fault insurance, covers your medical expenses and lost wages, regardless of who is at fault in an accident. It can also cover medical expenses for your passengers. This coverage is usually required in some states.

- Medical Payments Coverage (Med Pay): This coverage is similar to PIP, but it covers medical expenses for you and your passengers regardless of who is at fault in an accident, and it’s not limited to accidents with other vehicles. It’s often a good idea to have at least some Med Pay coverage, even if you have PIP.

Deductibles

A deductible is the amount of money you pay out-of-pocket before your insurance company starts paying for repairs or other covered expenses. The higher your deductible, the lower your premium will be. The lower your deductible, the higher your premium will be.

Choosing a deductible is a balancing act between cost and risk.

For example, if you have a $500 deductible for collision coverage and you’re in an accident that causes $2,000 in damage to your car, you’ll pay the first $500 and your insurance company will pay the remaining $1,500.

Understanding the Fine Print

Insurance policies can be complicated, so it’s important to read the fine print carefully. Pay attention to the following:

- Exclusions: These are specific situations or types of damage that your insurance policy doesn’t cover. For example, your policy may exclude coverage for damage caused by wear and tear or damage caused by driving under the influence of alcohol or drugs.

- Limits: These are the maximum amounts your insurance company will pay for certain types of coverage. For example, your liability coverage may have a limit of $100,000 per person for bodily injury and $300,000 per accident for property damage.

- Conditions: These are specific requirements you must meet in order to receive benefits from your insurance policy. For example, your policy may require you to report an accident to the police or to file a claim within a certain time frame.

Glossary of Common Insurance Terms

- Premium: The amount of money you pay to your insurance company for coverage.

- Policy: The contract between you and your insurance company that Artikels the terms of your coverage.

- Claim: A request for payment from your insurance company for covered losses.

- Beneficiary: The person or people who will receive the death benefit from a life insurance policy.

- Actuary: A professional who analyzes and predicts the likelihood of future events, such as accidents or deaths, and helps insurance companies set premiums.

Tips for Saving on Auto Insurance

You’re already taking the first step toward saving money on your auto insurance by researching your options. But there are plenty of other ways to reduce your premiums. Let’s dive into some tips that could help you save big on your auto insurance.

Discounts

Insurance companies offer a variety of discounts to lower your premiums. It’s like a game of “find the hidden treasures” in your insurance policy.

- Good Student Discount: If you’re a high-achieving student with good grades, you’re less likely to be involved in accidents. This translates to lower premiums for you.

- Safe Driver Discount: This is a no-brainer. If you’ve got a clean driving record, you’re rewarded with lower rates.

- Multi-Car Discount: Got more than one car? You can save on your insurance by bundling them together with the same company.

- Multi-Policy Discount: You’re not just a car owner, right? You’ve got a home, renter’s, or other insurance needs. Bundle them all together with the same company and watch those savings roll in.

- Anti-theft Device Discount: Have a car alarm, immobilizer, or other anti-theft devices? These features make your car less appealing to thieves, which means lower premiums for you.

- Defensive Driving Course Discount: Taking a defensive driving course can show you’re committed to being a safe driver. You’ll get a discount and learn valuable driving skills.

- Loyalty Discount: Sticking with the same insurance company for a while can earn you a discount. Loyalty is rewarded!

- Paperless Billing Discount: Going paperless is not just eco-friendly, it can also save you money on your insurance.

Improving Driving Habits

Remember that old saying, “Drive like you’re on a video game?” Well, in the real world, bad driving habits can cost you a lot more than just losing a virtual life.

- Avoid Distracted Driving: This one’s a biggie. Put down the phone, turn off the music, and focus on the road.

- Drive the Speed Limit: Speeding tickets are a surefire way to increase your insurance premiums.

- Maintain Your Vehicle: Regular maintenance can prevent breakdowns and accidents, which can save you money on insurance.

- Avoid Aggressive Driving: Tailgating, weaving through traffic, and road rage can all lead to accidents.

Avoiding Insurance Scams and Fraud

We’ve all heard stories about people getting scammed. Here’s how to protect yourself:

- Be Wary of “Too Good to Be True” Offers: If an insurance offer seems too good to be true, it probably is.

- Don’t Give Out Personal Information Over the Phone: Never give out your Social Security number or other sensitive information over the phone unless you’re absolutely sure you’re talking to a legitimate insurance company.

- Verify the Identity of Anyone You’re Dealing With: Ask for identification from anyone who comes to your home to discuss insurance.

- Read Your Policy Carefully: Know what your policy covers and what it doesn’t.

Driving Safety Courses

You’re probably thinking, “Safety courses? Aren’t those just for new drivers?” Think again. These courses can benefit drivers of all ages and experience levels.

- Enhanced Driving Skills: Learn new techniques for defensive driving, accident avoidance, and emergency maneuvers.

- Reduced Risk of Accidents: Studies have shown that drivers who complete defensive driving courses are less likely to be involved in accidents.

- Lower Insurance Premiums: Many insurance companies offer discounts to drivers who complete a certified driving safety course.

Concluding Remarks

So, who has the best auto insurance rates? The answer isn’t as simple as picking the lowest number on a list. It’s about finding the right balance between cost and coverage. By understanding the factors that influence your premiums, comparing different companies, and being smart about your coverage, you can get the best deal and drive with peace of mind.

Commonly Asked Questions: Which Company Has The Best Auto Insurance Rates

What are some common discounts I can get on auto insurance?

Insurance companies offer a variety of discounts, including good driver discounts, safe driver courses, multi-car discounts, and even discounts for having a good credit score.

How often should I review my auto insurance policy?

It’s a good idea to review your auto insurance policy at least once a year, especially if you’ve had any major life changes, like a new car, a move, or a change in your driving record.

Can I negotiate my auto insurance rates?

You can try to negotiate your rates, especially if you’ve been a loyal customer or if you’re bundling your insurance policies. Be prepared to shop around and have quotes from other companies to show them.