Daftar Isi:

Best car insurance rates Florida can be a challenge to find, but it’s essential to protect yourself and your vehicle. Florida’s unique driving environment, including high traffic volume and frequent weather events, significantly impacts car insurance costs. The Florida Department of Financial Services regulates the state’s insurance industry, ensuring consumer protection and fair practices. Understanding the factors that influence car insurance rates in Florida can help you navigate the process effectively.

From your driving history and age to the type of vehicle you own and your location, several factors contribute to your car insurance premium. Insurance companies use a complex algorithm to assess risk and determine rates based on these factors. By understanding how these factors work, you can make informed decisions to potentially lower your insurance costs.

Understanding Florida’s Car Insurance Landscape

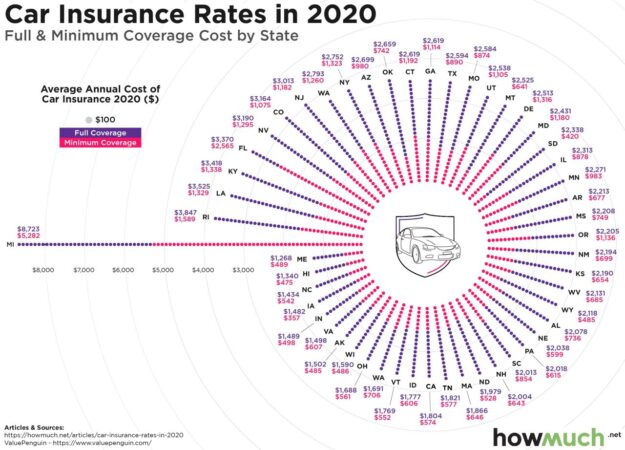

Florida’s car insurance market is unique and complex, influenced by a variety of factors that shape the cost of coverage for drivers. This complexity arises from the state’s high population density, susceptibility to natural disasters, and a legal environment that allows for significant claims.

Florida’s Unique Factors Influencing Car Insurance Rates

Florida’s car insurance rates are affected by several factors, including:

- High Population Density and Traffic Volume: Florida’s large population and high traffic density lead to a higher frequency of accidents, driving up insurance costs.

- Hurricane Risk: Florida’s vulnerability to hurricanes significantly increases the risk for insurers, as these storms can cause widespread damage to vehicles. This elevated risk is reflected in higher insurance premiums.

- Fraudulent Claims: Florida has a history of high levels of car insurance fraud, which drives up costs for all policyholders.

- “No-Fault” Insurance System: Florida operates under a “no-fault” insurance system, where drivers are required to file claims with their own insurer regardless of fault. This can lead to higher claims volumes and costs.

- High Litigation Rates: Florida has a high rate of car insurance lawsuits, further increasing costs for insurers.

The Role of the Florida Department of Financial Services

The Florida Department of Financial Services (DFS) plays a crucial role in regulating the state’s car insurance market. The DFS oversees insurance companies, ensuring they operate fairly and responsibly. This includes:

- Licensing and Supervision: The DFS licenses and supervises insurance companies operating in Florida, ensuring they meet financial stability and solvency requirements.

- Consumer Protection: The DFS protects consumers by investigating complaints against insurance companies and enforcing regulations.

- Rate Regulation: The DFS reviews and approves insurance rate filings, ensuring they are fair and reasonable.

Types of Car Insurance Coverage in Florida

Florida requires all drivers to carry a minimum level of car insurance coverage, including:

- Personal Injury Protection (PIP): This coverage pays for medical expenses, lost wages, and other related costs for the insured driver and passengers, regardless of fault.

- Property Damage Liability (PDL): This coverage pays for damages to other vehicles or property if the insured driver is at fault in an accident.

- Bodily Injury Liability (BIL): This coverage pays for medical expenses, lost wages, and other related costs for the other driver and passengers if the insured driver is at fault in an accident.

- Uninsured Motorist Coverage (UM): This coverage protects the insured driver and passengers if they are injured in an accident caused by an uninsured or underinsured driver.

- Collision Coverage: This coverage pays for repairs or replacement of the insured vehicle if it is damaged in an accident, regardless of fault.

- Comprehensive Coverage: This coverage pays for repairs or replacement of the insured vehicle if it is damaged by events other than an accident, such as theft, vandalism, or natural disasters.

Key Factors Determining Car Insurance Rates

Insurance companies in Florida, like elsewhere, use a complex system to determine car insurance premiums. They consider various factors to assess the risk of insuring a particular driver and vehicle. These factors play a significant role in shaping your insurance costs.

Driving History

A driver’s past driving record is a major factor in determining insurance rates. Insurance companies see a history of accidents, violations, and claims as an indicator of future risk. A clean driving record usually translates into lower premiums, while a history of accidents, traffic violations, or DUI convictions will likely result in higher rates.

Age

Age is a crucial factor influencing car insurance premiums. Younger drivers, especially those under 25, are statistically more likely to be involved in accidents. This increased risk is reflected in higher premiums. As drivers gain experience and age, their premiums generally decrease.

Vehicle Type

The type of vehicle you drive significantly impacts your insurance rates. Some vehicles are more expensive to repair or replace, making them riskier to insure. For example, luxury cars, sports cars, and high-performance vehicles often carry higher premiums than standard sedans or hatchbacks. Similarly, vehicles with advanced safety features like anti-lock brakes and airbags may qualify for discounts.

Location

Your location, specifically the zip code where your vehicle is garaged, can influence your insurance rates. Insurance companies consider factors like traffic density, crime rates, and the prevalence of accidents in specific areas. Areas with higher crime rates or more frequent accidents tend to have higher insurance premiums.

Credit History

In Florida, insurance companies are allowed to consider your credit history when calculating your car insurance rates. This practice is controversial, as some argue it is unrelated to driving ability. However, insurance companies maintain that individuals with good credit are more likely to pay their bills on time, including their insurance premiums.

Coverage Options

The amount and type of coverage you choose will impact your premiums. Comprehensive and collision coverage, which protect against damage to your vehicle from accidents and other incidents, are generally more expensive than liability coverage, which only covers damage to other vehicles or property.

Finding the Best Car Insurance Rates

Finding the best car insurance rates in Florida requires a strategic approach, involving careful research, comparison, and negotiation. While numerous factors influence your final premium, understanding these elements and utilizing effective strategies can significantly lower your insurance costs.

Comparing Quotes from Different Insurance Providers

Obtaining quotes from multiple insurance providers is essential for finding the best rates. This allows you to compare coverage options, premiums, and discounts offered by different companies. Here’s a step-by-step guide:

- Use Online Comparison Tools: Websites like Insurance.com, Bankrate, and NerdWallet provide convenient platforms for comparing quotes from various insurers. These tools streamline the process by collecting your information once and then presenting you with multiple quotes.

- Contact Insurance Providers Directly: Reach out to insurance companies directly through their websites or phone lines. This allows you to gather detailed information about their specific coverage options and discounts. Be sure to note any differences in coverage offered by each provider.

- Consider Local Insurance Agents: Independent insurance agents can provide personalized assistance by comparing quotes from multiple insurance companies. They can help you understand complex policies and recommend the best options based on your needs.

The Importance of Discounts and Coverage Options

While comparing quotes, carefully consider the discounts and coverage options offered by each insurance provider. These factors can significantly impact your final premium.

- Discounts: Insurance companies offer various discounts to reduce your premium. These discounts may be based on factors such as:

- Good Driving Record: Maintaining a clean driving record with no accidents or violations can significantly reduce your premiums.

- Safety Features: Vehicles equipped with safety features like anti-theft devices, airbags, and anti-lock brakes often qualify for discounts.

- Bundling Policies: Combining your car insurance with other insurance policies, such as home or renters insurance, can lead to significant savings.

- Membership Discounts: Some organizations offer discounts to their members. Check if you qualify for discounts through your professional associations, alumni groups, or other affiliations.

- Payment Options: Paying your premium annually or semi-annually instead of monthly can sometimes result in a lower rate.

- Coverage Options: Carefully evaluate the coverage options offered by each insurance provider. While comprehensive coverage may be more expensive, it provides greater protection against unexpected events. Consider your financial situation and risk tolerance when choosing coverage levels.

Negotiating Your Car Insurance Rate

Once you’ve compared quotes and identified a suitable provider, don’t hesitate to negotiate your rate. Insurance companies are often willing to work with customers to find a mutually beneficial solution.

- Highlight Your Positive Attributes: Emphasize your good driving record, safety features, and any relevant discounts you qualify for. This can demonstrate your low-risk profile and encourage the insurer to offer a lower rate.

- Shop Around Again: If you’re not satisfied with the initial offer, contact other insurance providers and compare their rates. This competitive approach can incentivize your chosen insurer to offer a better rate.

- Be Prepared to Walk Away: Don’t be afraid to walk away from a negotiation if you’re not comfortable with the terms. Having other quotes in hand gives you leverage to secure a more favorable deal.

Common Mistakes to Avoid: Best Car Insurance Rates Florida

Navigating the complex world of Florida car insurance can be daunting, and many drivers make mistakes that ultimately lead to higher premiums or inadequate coverage. Understanding these common pitfalls and taking proactive steps to avoid them is crucial for securing the best possible rates and ensuring you have the right protection.

Failing to Shop Around, Best car insurance rates florida

It’s a common misconception that all car insurance companies offer the same rates. The reality is that rates vary significantly from insurer to insurer. Failing to shop around and compare quotes from multiple companies can cost you hundreds, even thousands, of dollars annually.

- Example: Let’s say you’re currently paying $1,200 per year for your car insurance. By comparing quotes from three other insurers, you might discover a policy with similar coverage for $900 per year, saving you $300 annually.

Ignoring Discounts

Most insurance companies offer various discounts that can significantly reduce your premium. However, many drivers fail to take advantage of these savings opportunities.

- Common Discounts: Good driving record, safe driving courses, multiple car policies, homeownership, bundling insurance, and membership in certain organizations.

- Example: By taking a defensive driving course, you might qualify for a 10% discount on your premium, saving you $120 per year if your current premium is $1,200.

Not Understanding Your Coverage

Another common mistake is not understanding the different types of coverage available and choosing a policy that doesn’t adequately meet your needs.

- Example: If you have a leased or financed car, you’ll likely need comprehensive and collision coverage to protect your investment in case of an accident or damage. Failing to have this coverage could leave you financially responsible for significant repair costs.

Providing Inaccurate Information

When applying for car insurance, it’s crucial to provide accurate information about your driving history, vehicle, and other relevant details. Providing inaccurate information can lead to higher premiums or even policy cancellation.

- Example: If you misrepresent your driving record by failing to disclose a previous accident, you might be charged a higher premium when the insurer discovers the truth. In extreme cases, your policy could be canceled.

Not Reviewing Your Policy Regularly

Your insurance needs may change over time, especially if you make significant life changes such as getting married, having children, or purchasing a new car. Failing to review your policy regularly could result in insufficient coverage or paying for unnecessary coverage.

- Example: If you’ve recently paid off your car loan, you might be able to drop collision and comprehensive coverage, saving you money on your premium.

Resources and Tools

Navigating the complex world of car insurance in Florida can be daunting, but numerous resources and tools are available to help you find the best rates and make informed decisions. These resources provide valuable information, comparison tools, and guidance to ensure you secure the most suitable coverage at a price that fits your budget.

Online Car Insurance Comparison Tools

Online car insurance comparison tools are invaluable resources for Florida residents seeking the best rates. These platforms allow you to enter your information once and receive quotes from multiple insurance providers, simplifying the comparison process.

- Insurify: Insurify is a popular platform that compares quotes from over 20 insurance companies, providing a comprehensive overview of available options.

- Policygenius: Policygenius offers a user-friendly interface and allows you to compare quotes from various insurers, including major carriers and regional providers.

- The Zebra: The Zebra is another reputable comparison tool that aggregates quotes from numerous insurers, providing insights into pricing and coverage options.

These tools save you time and effort by streamlining the quote comparison process, allowing you to quickly identify the most competitive rates and coverage options.

Florida Department of Financial Services

The Florida Department of Financial Services (DFS) is a valuable resource for consumers seeking information about car insurance.

- Consumer Guides: The DFS website provides comprehensive consumer guides on car insurance, explaining coverage options, rights, and responsibilities.

- Complaints and Disputes: The DFS handles consumer complaints and disputes regarding car insurance, offering a platform for resolving issues with insurance providers.

- Financial Literacy Resources: The DFS offers financial literacy resources and educational materials to help consumers make informed decisions about insurance and other financial matters.

The DFS website is a reliable source of information and guidance for Florida residents seeking to understand their car insurance options and navigate the insurance landscape.

Florida Office of Insurance Regulation

The Florida Office of Insurance Regulation (OIR) is the state agency responsible for overseeing the insurance industry.

- Insurance Company Information: The OIR website provides information about licensed insurance companies operating in Florida, including financial stability ratings and complaint history.

- Consumer Protection Resources: The OIR offers consumer protection resources, including guides, publications, and FAQs on car insurance and other insurance products.

- Insurance Market Analysis: The OIR conducts market analysis and research on car insurance rates and trends in Florida, providing insights into the state’s insurance landscape.

The OIR website is a valuable resource for consumers seeking information about insurance companies, regulations, and market trends.

Independent Insurance Agents

Independent insurance agents represent multiple insurance companies, allowing them to provide personalized advice and tailored quotes.

- Broader Choice of Options: Independent agents can access a wider range of insurance products and carriers, providing more options to choose from.

- Expert Advice: Independent agents have extensive knowledge of the insurance market and can offer expert advice on coverage options and pricing.

- Personalized Service: Independent agents work with clients to understand their individual needs and recommend the most suitable coverage at a competitive price.

Working with an independent insurance agent can provide a personalized approach to finding the best car insurance rates and coverage options in Florida.

Conclusion

Finding the best car insurance rates in Florida requires careful research and comparison. By taking the time to understand the factors that influence rates, comparing quotes from different insurers, and considering discounts and coverage options, you can secure the most affordable and comprehensive car insurance policy. Remember to avoid common mistakes that can lead to higher premiums or inadequate coverage. Utilize available resources and tools to make informed decisions and ensure you have the right insurance protection.

Question Bank

How often should I review my car insurance rates?

It’s recommended to review your car insurance rates at least once a year, or even more frequently if your driving situation changes (e.g., new car, change in driving history, etc.).

What are some common car insurance discounts available in Florida?

Common discounts include good driver discounts, safe driver discounts, multi-car discounts, and bundling discounts for combining home and auto insurance.

What is the minimum car insurance coverage required in Florida?

Florida requires drivers to carry a minimum of $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL) coverage.