Daftar Isi:

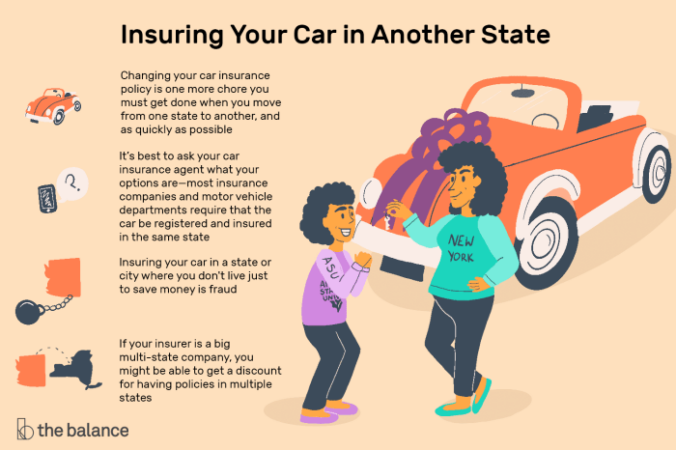

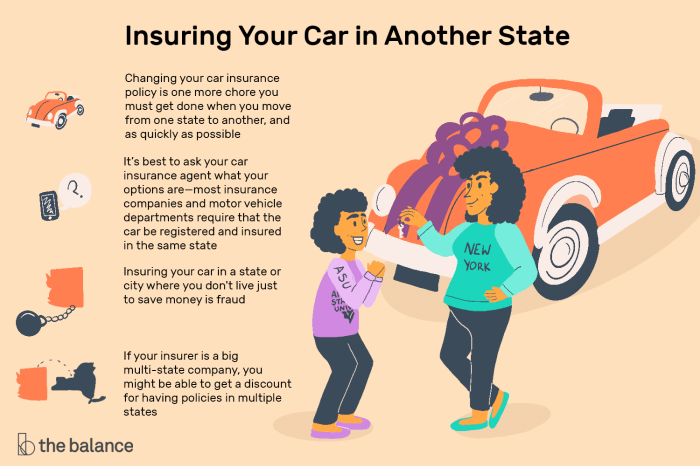

Can I insure a car registered in a different state? This question often arises when individuals move, purchase vehicles out of state, or simply want to explore insurance options across state lines. Navigating the world of car insurance can be complex, especially when dealing with interstate regulations. This article delves into the intricacies of insuring a vehicle registered in a different state, providing insights into state laws, insurance company policies, and essential factors to consider.

Understanding the rules governing car insurance across state lines is crucial for drivers. Each state has its own unique set of regulations, impacting the types of coverage required, the cost of insurance, and even the potential consequences of driving without proper insurance. Insurance companies also have their own policies regarding out-of-state vehicles, which can vary depending on factors such as the vehicle’s registration state, the driver’s history, and the specific coverage requested.

State Laws and Regulations

Each state in the United States has its own set of laws and regulations governing car insurance. These laws are designed to protect drivers, passengers, and pedestrians from financial hardship in the event of an accident.

The general rule is that you must have car insurance that meets the minimum requirements of the state where your car is registered. However, there are specific laws that may impact your ability to insure a car registered in another state.

State-Specific Requirements

The minimum car insurance requirements vary from state to state. For example, in some states, you may be required to have liability coverage, while in other states, you may also need to have collision and comprehensive coverage. You can find a list of minimum insurance requirements for each state on the website of your state’s Department of Motor Vehicles (DMV).

Here are some examples of state laws that may impact your ability to insure a car registered in another state:

- No-Fault Insurance: In no-fault states, drivers are required to carry personal injury protection (PIP) coverage, which covers their own medical expenses regardless of who is at fault in an accident. If you are driving a car registered in a no-fault state, you may be required to have PIP coverage even if your home state does not require it.

- Reciprocity Agreements: Some states have reciprocity agreements with other states, which means that drivers from those states can drive in their state without having to obtain a new driver’s license or insurance. However, these agreements do not always cover all types of insurance, so it is important to check with your insurance company to make sure you are covered.

- Insurance Verification: Some states require drivers to provide proof of insurance when they register their car. If you are driving a car registered in another state, you may need to provide proof of insurance that meets the requirements of the state where you are driving.

Consequences of Violating State Insurance Regulations

If you are caught driving without the required car insurance, you could face a number of consequences, including:

- Fines and Penalties: You may be fined for driving without insurance, and the amount of the fine may vary depending on the state and the severity of the offense.

- Suspension of Your Driver’s License: Your driver’s license may be suspended if you are caught driving without insurance.

- Impoundment of Your Vehicle: Your vehicle may be impounded if you are caught driving without insurance.

- Increased Insurance Premiums: If you are caught driving without insurance, your insurance premiums may increase in the future.

- Financial Responsibility: If you are involved in an accident without insurance, you could be held financially responsible for all damages, including medical expenses, property damage, and lost wages.

Insurance Company Policies

Insurance companies have different policies regarding out-of-state vehicle insurance. Some companies might readily insure vehicles registered in other states, while others may have limitations or specific requirements. Understanding these policies is crucial for individuals seeking insurance for vehicles registered outside their state of residence.

Factors Considered by Insurance Companies

Insurance companies evaluate several factors when determining eligibility and coverage for out-of-state vehicles. These factors include:

- State of Residence: The primary residence of the policyholder is a key factor. Some companies may only insure vehicles registered in states where they operate.

- Vehicle Usage: The purpose for which the vehicle is used (e.g., personal, commercial, business) can influence insurance coverage.

- Driving History: Past driving records, including accidents, violations, and claims, are reviewed to assess risk.

- Vehicle Value: The value of the vehicle plays a role in determining coverage amounts and premiums.

- State Regulations: Insurance companies must comply with regulations in the state where the vehicle is registered. These regulations may dictate minimum coverage requirements and other aspects of insurance policies.

Examples of Insurance Company Policies

Insurance company policies can vary widely. Here are examples of common policies related to out-of-state vehicle insurance:

- Full Coverage: Some insurance companies offer full coverage for vehicles registered in other states, including comprehensive and collision coverage. This coverage is typically available for vehicles used primarily for personal use and meet the insurer’s underwriting criteria.

- Limited Coverage: Other companies may only provide limited coverage for out-of-state vehicles, such as liability coverage. This approach may be common for vehicles used for commercial purposes or vehicles registered in states with different insurance requirements.

- State-Specific Requirements: Some insurance companies may have specific requirements for vehicles registered in certain states. For instance, they might require additional documentation or a higher deductible for vehicles registered in states with higher accident rates or stricter insurance regulations.

Types of Coverage

Car insurance offers various types of coverage to protect you and your vehicle in case of accidents, theft, or other unforeseen events. When insuring a car registered in a different state, understanding the coverage options available and how they might differ based on the registration state is crucial.

Coverage Options for Out-of-State Vehicles

The availability and cost of car insurance coverage can vary depending on the state where the vehicle is registered. Some states may have mandatory coverage requirements that differ from your home state. It’s important to check with your insurance company and the state’s Department of Motor Vehicles (DMV) to understand the specific requirements for your situation.

- Liability Coverage: This coverage is typically mandatory in most states and protects you financially if you cause an accident that injures someone or damages their property. It covers the other driver’s medical expenses, lost wages, and property damage.

- Collision Coverage: This coverage pays for repairs or replacement of your vehicle if it’s damaged in a collision, regardless of who is at fault.

- Comprehensive Coverage: This coverage protects your vehicle from damages caused by events other than collisions, such as theft, vandalism, hail, or fire.

- Uninsured/Underinsured Motorist Coverage: This coverage protects you if you’re involved in an accident with a driver who doesn’t have insurance or doesn’t have enough insurance to cover your damages.

- Personal Injury Protection (PIP): This coverage, often required in certain states, covers your medical expenses and lost wages if you’re injured in an accident, regardless of who is at fault.

- Medical Payments Coverage (Med Pay): This coverage provides medical payments for you and your passengers, regardless of fault, up to a certain limit.

- Rental Reimbursement: This coverage helps pay for a rental car while your vehicle is being repaired after an accident.

Variations in Coverage Availability and Cost

The availability and cost of coverage can vary based on the vehicle’s registration state.

- Minimum Liability Coverage Requirements: States have varying minimum liability coverage requirements. For example, some states may require higher liability limits than others.

- Availability of Optional Coverage: Some states may not require certain types of coverage, such as collision or comprehensive, but you can still purchase them as optional coverage.

- Cost of Coverage: Insurance rates can vary based on the state of registration due to factors such as the cost of living, traffic density, and the number of accidents in the area.

Example:

Let’s say you’re driving a car registered in California and you’re involved in an accident in Florida. Florida’s minimum liability coverage requirements might be higher than California’s. In this case, you may need to purchase additional liability coverage to meet Florida’s requirements.

Factors Affecting Insurability

Several factors beyond the car’s registration state can influence your ability to insure a car. Insurance companies carefully evaluate these factors to assess risk and determine your premiums.

Driver History

Your driving record plays a crucial role in determining your insurability. A clean driving history with no accidents, traffic violations, or DUI convictions is generally considered favorable. Conversely, a history of accidents, speeding tickets, or other violations can significantly impact your ability to get insurance or increase your premiums.

Insurance companies often use a system called a “risk score” to assess your driving history. This score is based on factors like the number and severity of your accidents, your driving experience, and your age. A higher risk score usually means higher premiums.

Vehicle Type

The type of car you drive also influences your insurability. Sports cars, luxury vehicles, and high-performance vehicles are often considered riskier to insure due to their potential for higher repair costs and a higher risk of accidents. Conversely, older, less expensive vehicles may be easier to insure, as they are typically associated with lower repair costs.

Location

The location where you live or drive can impact your insurability. Areas with higher crime rates, heavy traffic, or a higher number of accidents tend to have higher insurance premiums. This is because insurance companies are more likely to experience claims in these areas.

Consequences of Uninsured Vehicles

Driving without insurance is a risky decision that can have serious financial and legal repercussions. Not only can you face hefty fines and penalties, but you could also be held personally liable for any damages or injuries caused in an accident.

Financial Consequences

The absence of insurance can lead to significant financial burdens. Here are some examples:

- Fines and Penalties: Most states have strict laws requiring drivers to carry liability insurance. Fines for driving without insurance can range from hundreds to thousands of dollars, depending on the state and the severity of the offense. In some cases, you may also face license suspension or revocation.

- Liability for Damages: If you cause an accident without insurance, you’ll be personally responsible for covering all damages, including medical expenses, property repairs, and legal fees. This could result in substantial financial losses, especially if the accident involves serious injuries or significant property damage.

- Higher Costs in the Long Run: Even if you avoid an accident, driving without insurance can make it more expensive to obtain coverage in the future. Insurance companies often view drivers with a history of uninsured driving as high-risk, leading to higher premiums.

Legal Consequences

Driving without insurance can also have legal consequences, including:

- Criminal Charges: In some states, driving without insurance is considered a criminal offense. This could result in jail time, probation, or community service.

- Civil Lawsuits: If you cause an accident without insurance, the injured party can file a civil lawsuit against you. This could lead to a large financial judgment against you, even if you were not at fault for the accident.

- License Suspension or Revocation: Driving without insurance can lead to the suspension or revocation of your driver’s license, preventing you from legally driving. This can significantly impact your ability to get to work, school, or other essential activities.

Real-World Scenarios

Here are some examples of real-world scenarios where lack of insurance can lead to significant financial burdens:

- Accident Involving Injuries: Imagine you cause an accident that results in serious injuries to another driver. Without insurance, you could be held responsible for all medical expenses, lost wages, and pain and suffering. This could easily amount to hundreds of thousands of dollars, potentially leading to bankruptcy.

- Property Damage: You accidentally back into a parked car, causing significant damage. Without insurance, you’ll be responsible for the entire cost of repairs, which can be substantial depending on the vehicle’s make and model.

- Hit-and-Run: You’re involved in an accident but flee the scene without exchanging information. The police are able to identify you, and you’re charged with hit-and-run. In addition to criminal charges, you could face a civil lawsuit from the other driver, leaving you financially vulnerable.

Finding Insurance Options

Finding insurance for a car registered in another state can seem daunting, but it’s achievable with the right approach. By understanding your options and using effective strategies, you can secure comprehensive and affordable coverage for your vehicle.

Comparing Quotes from Multiple Providers

It’s crucial to compare quotes from several insurance companies to find the best deal. This ensures you’re not settling for a higher premium than necessary.

- Online comparison websites: These platforms allow you to enter your details and receive quotes from various insurers simultaneously, simplifying the process.

- Direct contact with insurance companies: Reach out to insurers directly to obtain quotes and discuss your specific needs.

- Insurance brokers: These professionals work with multiple insurance companies and can help you find the best coverage at competitive rates.

Registration and Licensing Requirements: Can I Insure A Car Registered In A Different State

When insuring a car registered in a different state, understanding the registration and licensing requirements is crucial. These requirements can significantly impact your insurance coverage and even determine whether you can legally drive the vehicle.

Registration Requirements, Can i insure a car registered in a different state

The registration process for vehicles varies across states. Each state has its own set of rules and regulations governing the registration of vehicles, including:

- Proof of ownership: You must provide evidence that you own the vehicle, such as a title or bill of sale.

- Vehicle inspection: Some states require a safety inspection before you can register a vehicle. This ensures the vehicle meets minimum safety standards.

- Payment of registration fees: States charge registration fees based on factors like vehicle type, age, and weight.

- Proof of insurance: Many states require you to provide proof of insurance before you can register a vehicle. This ensures that you have financial protection in case of an accident.

Licensing Requirements

Similarly, licensing requirements for drivers also vary across states. These requirements typically include:

- Driver’s license: You must possess a valid driver’s license from the state where you reside. However, some states may have reciprocity agreements that allow you to drive with a license from another state.

- Driving history: Your driving history, including any traffic violations or accidents, may be reviewed during the licensing process.

- Proof of residency: You may need to provide proof of residency in the state where you are applying for a driver’s license.

Impact on Insurance Coverage

Registration and licensing requirements can impact your insurance coverage in several ways. For instance:

- Proof of insurance requirement: If a state requires proof of insurance for registration, you may need to obtain insurance from an insurer licensed in that state. This ensures that your insurance coverage is valid in the state where your vehicle is registered.

- Coverage limitations: Some insurance companies may limit the coverage they offer for vehicles registered in other states. This may include restrictions on the types of coverage available or the amount of coverage provided.

- State-specific requirements: Certain states have specific requirements regarding insurance coverage, such as minimum liability limits or mandatory coverage for certain types of vehicles. You need to ensure that your insurance policy meets these requirements.

Examples of State Variations

Here are some examples of how registration and licensing requirements can vary across states:

- California: Requires a smog check for vehicles registered in the state.

- Texas: Requires a safety inspection for vehicles registered in the state.

- New York: Requires proof of insurance for registration and has a no-fault insurance system.

Closure

Insuring a car registered in a different state can be a challenging but manageable process. By understanding the interplay of state laws, insurance company policies, and individual factors, drivers can navigate this complex landscape and secure appropriate coverage. Remember to research your options thoroughly, compare quotes from multiple insurers, and consult with an insurance agent for personalized advice. Staying informed and proactive ensures you have the necessary protection on the road, regardless of where your vehicle is registered.

Questions Often Asked

What are the general rules regarding car insurance in different states?

Each state has its own set of car insurance regulations, including minimum coverage requirements, types of coverage offered, and penalties for driving without insurance.

Can I use my current insurance provider to insure a car registered in another state?

Many insurance companies offer coverage for vehicles registered in different states, but you should contact your current provider to confirm their policies and coverage options.

What factors influence the cost of insurance for an out-of-state vehicle?

Factors like the vehicle’s make and model, the driver’s history, the vehicle’s location, and the state’s insurance regulations can affect the cost of insurance.

What are the consequences of driving an uninsured vehicle registered in another state?

Driving an uninsured vehicle can result in fines, license suspension, and potential legal liabilities in case of an accident.