Daftar Isi:

Florida car insurance rate increase 2023 has become a hot topic, with drivers across the state feeling the pinch of higher premiums. This surge in costs is a result of several factors, including inflation, rising repair costs, and an increase in claims frequency. As the Sunshine State grapples with this financial burden, understanding the causes and potential solutions is crucial for both drivers and the insurance industry.

The Florida car insurance market is a complex ecosystem, influenced by various factors. The state’s unique legal landscape, including no-fault insurance and the ability to sue for pain and suffering, has contributed to a higher frequency of claims compared to other states. Additionally, the prevalence of fraudulent claims and lawsuits has also put upward pressure on premiums.

Florida Car Insurance Market Overview

The Florida car insurance market is a complex and dynamic environment characterized by high insurance premiums, a high volume of claims, and intense competition. The state’s unique demographics, weather patterns, and legal framework significantly influence the market’s trajectory.

Florida’s high population density, coupled with a significant influx of tourists, leads to a higher number of vehicles on the road, increasing the likelihood of accidents. Moreover, the state’s warm climate and frequent severe weather events, such as hurricanes and thunderstorms, contribute to a higher incidence of property damage and personal injury claims.

The Competitive Landscape

The Florida car insurance market is highly competitive, with numerous national and regional insurers vying for market share.

The top five insurers in Florida, based on market share in 2022, are:

- State Farm

- GEICO

- Progressive

- Universal Insurance

- Allstate

These insurers compete aggressively on price, coverage options, and customer service. The intense competition has led to a trend of lower premiums in recent years, particularly for drivers with good driving records and clean claims histories.

Impact of Recent Legislative Changes and Regulatory Updates

The Florida Legislature and the Florida Office of Insurance Regulation (OIR) have implemented numerous changes in recent years to address the challenges facing the car insurance market.

One significant change was the passage of Senate Bill 2A in 2021, which aimed to reduce fraud and abuse in the personal injury protection (PIP) system. The bill made several changes to the PIP system, including:

- Limiting the amount of medical benefits available under PIP coverage

- Requiring insurers to offer lower-cost PIP options

- Strengthening anti-fraud measures

These changes are expected to have a significant impact on the market, potentially leading to lower premiums and a more stable insurance environment.

Factors Contributing to Rate Increases

Florida’s car insurance rates have been on the rise in recent years, impacting drivers across the state. Several factors contribute to these increases, making it crucial to understand the driving forces behind them.

Inflation and Repair Costs

Inflation plays a significant role in driving up car insurance rates. Rising costs for vehicle parts, labor, and medical care directly impact insurance premiums. When repair costs increase, insurance companies need to charge higher premiums to cover these expenses. For instance, the cost of a new car has risen dramatically in recent years, leading to higher payouts for total loss claims.

Increased Claims Frequency

Another contributing factor is the increased frequency of car accidents and claims. This rise in claims can be attributed to various factors, including:

- Increased traffic volume and congestion, leading to more accidents.

- Distracted driving, such as texting or using mobile devices while driving.

- Aggressive driving behaviors, such as speeding and tailgating.

As claims frequency increases, insurance companies face higher payouts, forcing them to raise premiums to maintain profitability.

The Impact of Litigation

Florida’s legal environment also contributes to higher insurance rates. The state has a high number of lawsuits related to car accidents, often involving claims for pain and suffering. This litigation environment can lead to higher payouts for insurance companies, which are then passed on to policyholders in the form of increased premiums.

Impact of Different Factors on Rate Increases Across Regions

The impact of these factors on rate increases can vary across different regions of Florida. For example, areas with higher population density and traffic volume may experience more frequent accidents, leading to higher insurance rates. Similarly, regions with a higher cost of living may face higher repair costs, further driving up premiums.

Impact on Drivers and Consumers

The surge in Florida car insurance rates has a significant impact on drivers and consumers, affecting their financial well-being and access to essential insurance coverage. Rising premiums translate into a substantial financial burden for many individuals and families, especially those already struggling with economic challenges.

Financial Burden on Drivers

The escalating car insurance costs in Florida place a considerable strain on drivers’ budgets. Drivers are forced to allocate a larger portion of their income towards insurance premiums, leaving less money for other essential needs, such as housing, food, healthcare, and education. This financial pressure can lead to difficult choices, potentially forcing individuals to cut back on other expenses or even delay necessary medical treatments or car repairs.

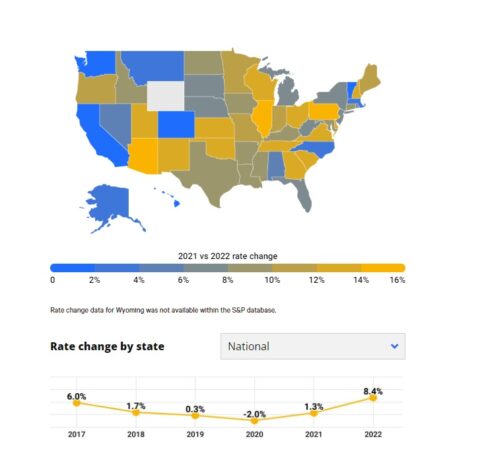

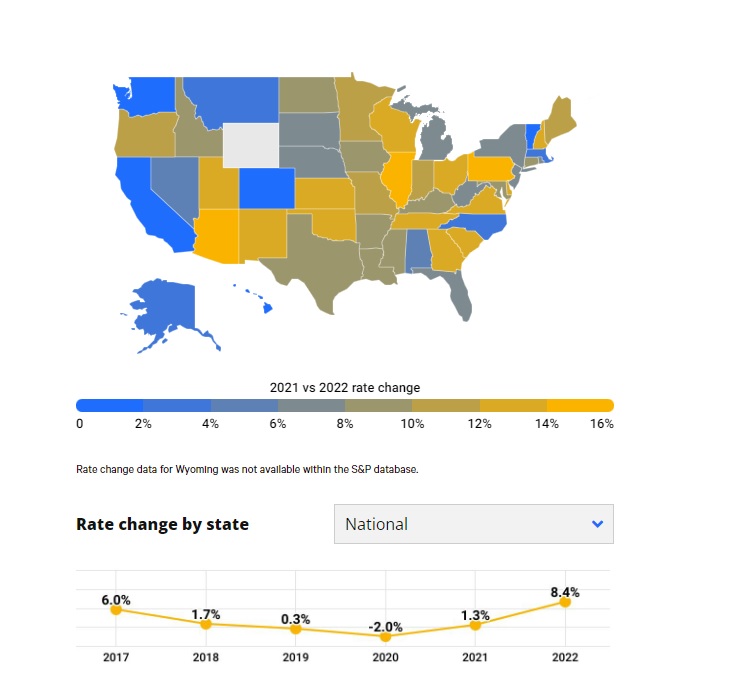

The average car insurance premium in Florida has increased by over 20% in the past two years, according to the Florida Office of Insurance Regulation. This means that a driver who previously paid $1,000 annually for car insurance may now be paying $1,200 or more.

Impact on Affordability and Access to Insurance, Florida car insurance rate increase 2023

The affordability of car insurance is becoming a major concern for many Floridians, particularly low-income families and individuals. Rising premiums can make it difficult for some drivers to afford adequate coverage, leading to potential financial hardship in the event of an accident. This situation may also force some drivers to choose cheaper, less comprehensive coverage options, leaving them vulnerable to significant financial losses in the event of a major accident.

A study by the National Association of Insurance Commissioners (NAIC) found that nearly one in five drivers in the United States is uninsured, with the highest rates of uninsured drivers concentrated in states with high insurance costs.

Strategies for Drivers to Mitigate Rate Increases

Drivers can employ several strategies to mitigate the impact of rising car insurance rates.

- Shop around for better rates: Compare quotes from multiple insurance companies to find the best rates and coverage options. Online comparison tools can make this process easier and more efficient.

- Improve driving record: Maintain a clean driving record by avoiding traffic violations and accidents. Good driving habits can significantly reduce insurance premiums.

- Increase deductibles: Consider increasing deductibles to lower monthly premiums, but ensure that the deductible amount is affordable in the event of an accident.

- Bundle insurance policies: Combine home, auto, and other insurance policies with the same company to qualify for potential discounts.

- Take advantage of discounts: Explore available discounts, such as those for good students, safe drivers, and multi-car policies.

Industry Response and Future Outlook: Florida Car Insurance Rate Increase 2023

The Florida car insurance market is experiencing significant challenges due to rising rates, prompting a multifaceted response from the industry. Insurance companies are actively seeking solutions to address affordability concerns while navigating the complexities of a rapidly evolving landscape.

Efforts to Address Affordability Concerns

Insurance companies are implementing various strategies to mitigate the impact of rising rates on consumers.

- Discount Programs: Many insurers are expanding their discount programs, offering incentives for safe driving, good credit, and other factors that can reduce risk. These programs can help make insurance more affordable for eligible policyholders.

- Payment Plans: Some insurers are offering flexible payment plans and installment options to make premiums more manageable for policyholders. These options can help spread out the cost of insurance over time, making it easier for individuals to afford coverage.

- Community Outreach: Insurance companies are increasing their community outreach efforts, providing educational resources and guidance to help consumers understand their insurance options and make informed decisions. This can help empower consumers to find more affordable coverage.

Potential Future Trends in Florida Car Insurance Rates

Predicting future trends in car insurance rates requires careful consideration of several factors, including legislative changes, economic conditions, and the severity of claims.

- Legislative Reforms: The Florida legislature is actively considering reforms aimed at addressing the affordability of car insurance. These reforms could impact rates, potentially leading to either increases or decreases depending on the specific measures implemented.

- Economic Conditions: Inflation and rising costs of repairs can influence the cost of insurance. Economic downturns may lead to increased claims frequency, potentially pushing rates higher.

- Severity of Claims: The number and severity of accidents can significantly impact insurance rates. Increased claims frequency or higher repair costs can drive up premiums.

Long-Term Implications for the Florida Insurance Market

The ongoing rate increases have significant implications for the long-term health of the Florida insurance market.

- Consumer Affordability: Rising rates could make insurance unaffordable for some consumers, potentially leading to increased uninsured drivers and a decline in coverage penetration.

- Market Stability: If rates continue to climb, it could lead to insurer insolvencies and a decrease in competition within the market. This could result in higher premiums and fewer options for consumers.

- Policyholder Behavior: High rates could incentivize policyholders to seek lower coverage limits or drop coverage altogether. This could lead to a decline in the overall financial security of the market.

Summary

The future of Florida car insurance rates remains uncertain, with a multitude of factors influencing their trajectory. The insurance industry is actively seeking solutions to address affordability concerns, including stricter fraud prevention measures and innovative pricing models. While the outlook for drivers is not entirely clear, understanding the underlying causes and the industry’s response is crucial for navigating this evolving landscape.

Question Bank

What are the main reasons for the increase in Florida car insurance rates?

Several factors contribute to the rise in car insurance rates, including inflation, increased repair costs, rising claims frequency, and fraudulent claims.

How do I find the best car insurance rates in Florida?

Compare quotes from multiple insurance providers, consider increasing your deductible, and look for discounts for good driving records and safety features.

Are there any steps I can take to reduce my car insurance costs?

Yes, you can shop around for better rates, improve your driving record, and consider safety features in your vehicle.

What are the long-term implications of rising car insurance rates?

Rising car insurance rates could make car ownership less affordable, especially for low-income families, and potentially lead to an increase in uninsured drivers.